Once again, the politicians in Washington have chosen to attack the straw man of the tax code. They love to portray the IRS as somehow (they never state this but artfully imply it) creating the tax code. The truth is quite the opposite: Whenever a constituent darkens a member of Congress’s doorway asking for something in return for a campaign contribution, the result is frequently a new provision in the tax code if the contribution or contribution bundle was big enough. Every few years, we go through a purging of the code in the interest of “lowering your taxes” or “making it simpler” but the net result is just a reset in this interaction between Congress and constituents.

This year, part of simplification in legislation that would affect your taxes in 2018 is decreasing the number of tax rate brackets from seven to three. At the same time, various deductions would be eliminated such as the homeowner’s (a special interest group if there ever was one!) mortgage interest deduction and caps on charitable contributions (charities are another “special interest” — a term we’ve all been trained to hate — with powerful lobbies in Washington). The minimum rates commonly discussed would be an increase from 10% to 12% at the bottom.

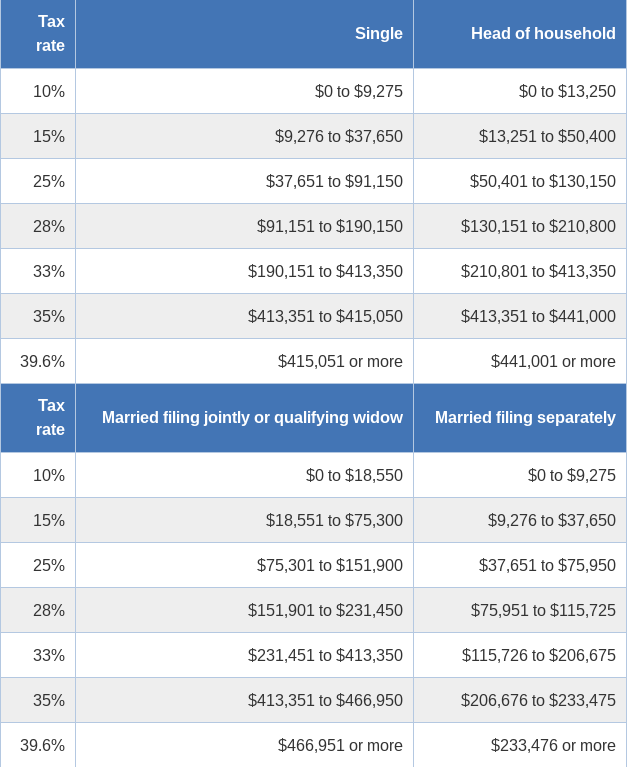

Another aspect of the so-called simplification is the sought-after decrease in statuses from four to two: Head of Household and Widow/Widower would be eliminated. The following chart shows the current state of complexity.

What this dialogue ignores is that the complexity of the tax code is in two areas that precede or follow the determination of this rather mechanical and simple process: What is the income amount to be taxed and what credits are available to lower the amount of tax once it has been calculated. The former we call determining adjusted gross income (or AGI) while the latter consists of subtracting various calculated amounts from what would otherwise have been the tax to be paid. In many cases, for those able to take advantage of the nuances of the tax code, they can lower their tax due to zero (especially corporations)!

What this dialogue ignores is that the complexity of the tax code is in two areas that precede or follow the determination of this rather mechanical and simple process: What is the income amount to be taxed and what credits are available to lower the amount of tax once it has been calculated. The former we call determining adjusted gross income (or AGI) while the latter consists of subtracting various calculated amounts from what would otherwise have been the tax to be paid. In many cases, for those able to take advantage of the nuances of the tax code, they can lower their tax due to zero (especially corporations)!

If the only complexity in Title 26 of the United States Code (the formal name for the tax code) were just what politicians are trying to con us with, their proposal would be relevant. But, I’ll bet that most readers, once they know their AGI, can place themselves in the chart in less than 15 seconds. Are you married or single? Is your spouse dead or alive? If you are single, do you have dependents? Then, how much is your AGI? Voila! Read to the left on the chart above, and that’s the rate by which to multiply your AGI.

As always with tax policy changes, there are winners and losers. Early betting on potential losers is on single mothers who will lose the benefit of preferential treatment. Congressional staffers though have been quick to point out that more generous child care deductions will more than offset the double whammy that some have identified — an increase in tax rates, remember the increase from 10% to 12% at the bottom, and the loss of the household deduction built into their status (income not taxable until $13,250). We’ll keep an eye on the childcare deduction as will Forbes and others.

If you work with us, however, your taxes will, in each succeeding year, be increasingly lowered by credits as much as your circumstances will allow — we seek to structure your financial life to gain access to credits or to shield income, legally, from taxation. And that’s not simple, nor is it going to be, at least not for long. Why? Well, that’s where we started. Remember that person darkening the Congress member’s doorway?

We are working on an update to this article. Look for it soon.